累退稅

例子

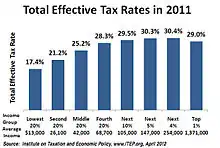

銷售稅、增值稅、燃油稅等基於日常開支實際消耗而徵收的稅項多被認為是累退稅。雖然隨收入和財富增加,日常開支會隨之而上升,但這些衣、食、住、行的開支佔整體收入的比率,當收入達到一定金額之後,卻不升反跌。由於這稅率多為固定稅率,所以納稅人的實際稅率亦相對下跌。

參考

- (PDF). Citizens for Tax Justice. 12 April 2012 [2013-06-04]. (原始内容存档 (PDF)于2020-06-13).

- Webster (页面存档备份,存于) (3): decreasing in rate as the base increases (a regressive tax)

- American Heritage 的存檔,存档日期2008-06-03. (3). Decreasing proportionately as the amount taxed increases: a regressive tax.

- Dictionary.com (页面存档备份,存于) (3).(of tax) decreasing proportionately with an increase in the tax base.

- Britannica Concise Encyclopedia (页面存档备份,存于): Tax levied at a rate that decreases as its base increases.

- Sommerfeld, Ray M., Silvia A. Madeo, Kenneth E. Anderson, Betty R. Jackson (1992), Concepts of Taxation, Dryden Press: Fort Worth, TX

This article is issued from Wikipedia. The text is licensed under Creative Commons - Attribution - Sharealike. Additional terms may apply for the media files.